China Continues Dominating world vehicle production

China will remain the primary driver of global production growth over the next four years, but the U.S. will remain the No. 2 vehicle producer in the world as North America continues to play a unique role in the automotive industry.

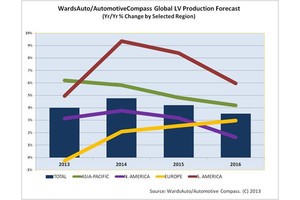

The WardsAuto /AutomotiveCompass report comes from the new released joint Global Light Vehicle and Powertrain Forecast service from two well respected sources of automotive data and analysis companies. The forecast calls for auto makers to consolidate the number of platforms underpinning their vehicles while increasing the percentage of cars and trucks that rely on smaller engines.The WardsAuto /AutomotiveCompass forecast projects growth in all global regions through 2018, with total vehicle output increasing 23 percent over the next six years.

The report highlights the China-led Asia-Pacific region’s increasing dominance, especially through 2016, when production in China alone will climb to a stunning 26 million units. Which is a 7.5 million unit increase from last year’s production numbers.

By comparison, production in the U.S., the No. 2 vehicle producer, is projected to increase by only 1.3 million over the same time period. This represents only about 17% of Chinas projected growth.

Production in the third-highest producing country, Japan, is forecast to decline by 875,000 units over the next four years, as capacity continues to shift to other locations.

In that same period, India will surge ahead of South Korea and Germany to rank fourth among vehicle producing countries.

The outlook projects that Volkswagen will lay claim to the top-produced platform in the world, by 2015, as its MQB architecture, which will spawn several small and midsize car and cross/utility vehicles. This should end a three-year reign by Toyota’s MC platform that began last year (when it usurped Hyundai’s HD architecture) and is expected to continue through 2014.

The forecast confirms the gradual production consolidation trend among global platforms. In 2012, 31 platforms accounted for half of global production. In 2016, that number drops to 27.

The WardsAuto/AutomotiveCompass global powertrain forecast also shows the shift to smaller engines continuing as production of vehicles with engines of 4-cylinders or less rises from 82 percent of the total in 2012 to 85% in 2018. Ironically, as North America remains a bastion for larger engines, it will lead the growth of smaller engines. North American production of vehicles with engines of 4 cylinders or less increases from 47 percent of the region’s total in 2012 to 55 percent in 2018.

The new WardsAuto/AutomotiveCompass Global Automotive Light Vehicle and Powertrain Forecast, covering over 98% of the global manufacturing base, is available immediately to subscribing clients.